TWO GREEDY HOGS GAVE us the 2008 Wall St. CRASH, HOMELESSNESS for many, INFLATION and DOUBLING of RENTS, UTILITIES and FOOD COSTS for ALL OF US!

NYC #2948692-21-111

NYC #2948692-21-112

HOW IN THE HELL did George W. Bush pick two brigands like these guys?

W is showing up as another sub-moronic Herbert Hoover -- He picked

the very two top appointees who were guarantee to steer the nation over

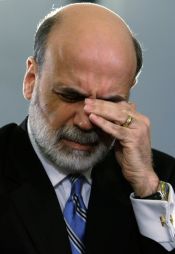

the waterfall crashing on the rocks of a Great Depression. ![]()

The first bozo, on the left, Hank Paulson, a top level financier,

insured

that Washington's eventual rescue policies would concentrate on trying

to bail-out Wall Street while ignoring the gnawing cancer

of its warped ambitions and financial malpractices. The second, an economics

professor whose SPECIALTY WAS the 1929 DEPRESSION fergawdsakes! Totally

misapplied dogma about how to guard against severe downturns! Like getting

WERNER BRAUN billions to BUILD then crash inside the CHALLENGER! Bernanke

did not understand the criminality of WALL STREET, its financial recklessness

or saw the gathering global inflation and just lied and said the Emperor

had a fine suit of clothes on and would he like another just like it?

Another one just

like it? Okaaay.

You're hired!

Henry Paulson, Bush's pick as treasury secretary, was not your ordinary gray-flannel investment bank CEO. He was MONEY MAD. MONEY DRUNK. MONEY INTOXICATED. One 2006 Business Week article spotlighted the new secretary as a high-roller: "Think of Paulson as Mr. Risk. He's one of the key architects of a more daring Wall Street where securities firms are taking greater and greater chances in their pursuit of profits." That, the magazine added, "by risks, we mean taking on more debt ... it means placing big bets on all sorts of exotic derivatives and other securities." That means stuff like collateralized debt obligations (CDOs) and credit default swaps (CDSs), innovations we now know to have spread toxicity, opacity, MISTRUST and finally, paralysis and a death rattle.

The SECOND BRIGAND is a legit Economics professor -- Ben Bernanke, who before replacing Alan Greenspan as Federal Reserve Board chairman in early 2006. He had served almost three years as the Chairman of George W. Bush's Council of Economic Advisers. There he had been a cheerleader for Bush economic policies, including upper-bracket tax cuts, Social Security privatization, "securitization" of assets and "safe" financial derivatives. On top of which, he was an academic and theoretical specialist in monetary policy and economic depressions - a man who boasted of understanding downturns' critical preventative. The Fed should pump up the money supply or liquidity which would overcome any credit crunch. As a card-carrying monetarist, he also insisted there was no meaningful inflation during the 2005-2007 period even though global commodity price indexes had been soaring.

Thus, and without knowing it, did an inept George W. Bush assemble his two chief architects of neo-Hooverism but we know W couldn't tie his shoes without help. Be certain that CHENEY sent them in, and that BUSH SENIOR told CHENEY to do it as BUSH Senior is and always has been on top of the two puppets in the White House as well as intimately connected with WALL STREET. These two Banksters would pick up where the original Disasterman, Alan Greenspan, Fed Chairman between 1987 and early 2006, had left off. Together, alas, the two would steer U.S. policy towards false pretenses, panic and economic disaster - Old Hoover outcomes re-achieved through new biases, ideology and myopia.

Wall Street's "Mr. Risk," calling the shots at Treasury, would focus the Bush administration's 2008 economic "rescue" policies not on the broad national interest but on bailing-out the "Frankenstein Fifteen" top U.S. financial institutions - the big five investment firms, the five largest commercial banks, the four mortgage biggies, and AIG, the rogue insurance giant. Along with the buccaneering hedge funds, these were the big firms that borrowed huge sums, merged grandiosely,, experimented with all "the exotic derivatives and other securities" and led the multi-trillion-dollar metastasis through which finance ballooned to take over domination of the U.S. economy by 2004 with 20-21% of the U.S. Gross Domestic product. Although in mid-2007, Paulson pretended that the emerging crisis involved no more than bad real estate lending practices, the cynical observer can assume that "Mr Risk," the arch-insider, knew what he was covering up - how deeply the malpractice and deception ran -- and on whose behalf.

If Paulson wanted to keep the spotlight off the real culprits -- the Frankenstein financial and mortgage banker laboratories, with their several trillions of exotic mortgages, toxic CDOs and Las Vegas-like credit swaps -- then narrow-gauge academician Bernanke at the Fed was the perfect sidekick. The economic ivory-tower theory in which Bail-out Ben had immersed himself for thirty years ignored 21st century mega-innovations and looked back seven decades to the Crash of the 1930s and how that long-ago debacle might have been prevented.

Alas, poor Ben -- his economist heroes have long been Milton Friedman and the latter's wife, Anna Schwartz, who some four decades ago co-authored a landmark volume entitled A Monetary History of the United States. On October 18, 2008, in a prominent interview published by the Wall Street Journal, Anna Schwartz opined that Bernanke was simply getting Fed policy wrong. The problem does not lie with the money supply or liquidity as it did in the 1930s. It lies with all these toxic securities the Wall Street geniuses dreamed up, gorged on, and sold around the globe in huge quantities between 2003 and 2007. "They're toxic," says Ms. Schwartz, "because you cannot sell them, you don't know what they're worth, your balance sheet is not credible, and the whole market seizes up." In fact, by giving transfusions to otherwise insolvent banks, Paulson and Bernanke have prolonged the crisis: "They should not be recapitalizing firms that should be shut down ... Firms that made wrong decisions should fail." That, of course, was how it worked in the old days when "creative destruction" kept capitalism on its toes. Now, of course, it's on its butt.

If Paulson and Bernanke had been willing to take a reformist blowtorch to the big fifteen and their practices and products back in late 2007 or early 2008, some six or eight might well have had to be dismantled, taken over or forced into bankruptcy or receivership, but the stock market and credit crisis of the last few months might been avoided or greatly mitigated. Instead, Paulson pretended that nothing serious was wrong because he came out of the same Wall Street ego-trip, and Bernanke could not transcend his student-of-the- 1930s academic background. "This was [his] claim to be worthy of running the Fed," says Anna Schwartz. However, Bernanke flubbed because he was fighting the last war, not the present one.

Worse still, the policies that Paulson and Bernanke did implement at such staggering cost have only begun to do their full long-term damage, which will probably come in a round of even more serious inflation. Together, the Treasury and the Fed have spent or loaned over a trillion dollars in financial-sector aid. As set out by economist Brad Setser of the Council of Foreign Relations, besides steering $950 billion into the U.S. financial system ($500 billion sent over by the Treasury), the Fed has provided still another $450 billion of dollar liquidity to European central banks to spread around on that continent. This decision by the United States to be the lender of last resort, in tandem with Washington's late September and October scare rhetoric about U.S. and world economy seizing up unless Congress passed the Paulson-Bernanke bail-out plan, has internationalized the crisis and made the U.S. dollar the pretended currency of the rescue instead of the vulnerable currency of the underlying problem. Something similar happened back in August 2007, when for 4-5 weeks a flight to "safety" and U.S. treasury debt buoyed the U.S. dollar. September and October have brought this result on an even larger scale.

Administration economists have said not to worry. This trillion won't be inflationary because that effect will be lost amid the 2008 assets deflation. This is probably more bunk from economic experts who have been right about practically nothing in the last few years. Global commodity indexes have been rising since 2003, although carefully crafted federal statistics kept that pressure from being acknowledged in the U.S. until 2008. Now the common wisdom is that declining commodity prices spell a long-term decline. The better likelihood is that inflation, still much in evidence globally, is only taking a breather, as it did circa 1971 and circa 1974 during the 1967-1980 inflation cycle. Within a matter of months, Washington's huge 2008 borrowing and soon-to-be-record trillion-dollar budget deficits will send inflation to new heights, and the current "treasuries bubble" and "U.S. dollar bubble" will pop.

Indeed, Ben Bernanke must remember from his old research that in the Spring of 1933, even after the huge assets deflation of 1929-32, new President Franklin D. Roosevelt's talk about cheap money, stimulus and reflation quickly sent commodity prices and inflation climbing. And today's rampant loan-making and deficit economics, by comparison, promise to make the FDR of 1933 look like Ebenezer Scrooge. Neo-Hooverism, in contrast to the 1929-32 version, is coming out of a new playbook.

The original, undoctored text under two or three comments by me was by Kevin Phillips who has a book Bad Money: Reckless Finance, Failed Politics and the Global Crisis of American Capitalism, published by Viking. The words hog, felon, moron, money-intoxicated and death rattle were my additions.

<===== BACK TO THE WHISPER WEBPAGE

<=====

BACK TO THE AMERICAN MELTDOWN WEBPAGE